Wind and solar capacity in south-east Asia climbs 20% in just one year, report finds.

In a significant stride towards sustainable energy, the Association of Southeast Asian Nations (ASEAN) has witnessed a remarkable increase in its renewable energy capacity. A recent report from Global Energy Monitor (GEM) reveals a 20% surge in wind and solar capacity across the region in 2023 alone, pushing the total to an impressive figure of over 28 gigawatts (GW).

RELEVANT SUSTAINABLE GOALS

This leap marks a pivotal moment in ASEAN’s energy landscape, demonstrating a growing commitment to renewable sources. These technologies now account for 9% of the electricity generating capacity in countries like Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam. This shift not only reflects the region’s dedication to sustainable practices but also aligns with global efforts to combat climate change.

Current State of Renewable Energy in ASEAN

The landscape of renewable energy within the ASEAN region is undergoing a dynamic transformation. As of 2023, solar and wind technologies have begun to leave a substantial mark on the region’s energy mix. Collectively, these renewable sources now compose 9% of the total electricity generating capacity across the ASEAN countries. This figure is more than just a statistic; it’s a testament to the region’s escalating shift towards sustainable energy practices.

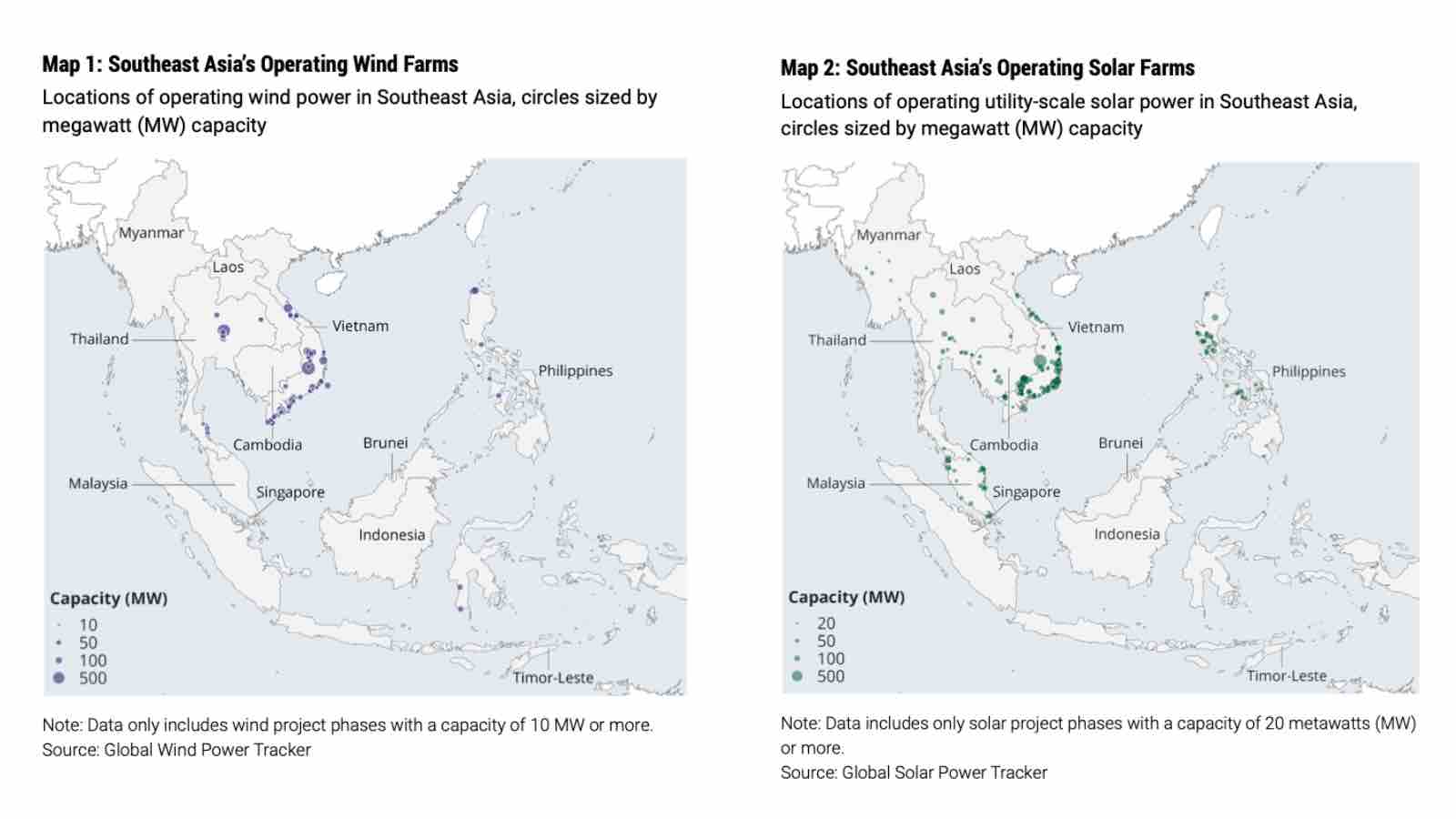

Vietnam, with a prospective capacity exceeding 86GW, including 72GW from offshore wind, faces challenges in realizing this potential. Currently, only 2% of this capacity is under construction, hindered by a lack of clear and reliable renewable energy policies. Additionally, GEM considers approximately 40GW of utility-scale solar and wind projects in Vietnam as “shelved,” due to a lack of progression or announcements in the past two years. Despite these setbacks, Vietnam is actively pursuing a just energy transition partnership (JETP) with developed countries and has released its latest national electricity development plan for 2021–2030, known as the power development plan 8 (PDP8). However, the impact of these policy alignments and funding schemes remains to be seen.

The Philippines stands out in the ASEAN region, responsible for 45% of the anticipated capacity. The country’s Green Energy Auction Program (GEAP) is set to facilitate over 11GW of renewable energy development. In its March 2023 auction, the Philippines secured bids for 3GW of solar, onshore wind, and bioenergy projects, with start dates between 2024 and 2026. Although this fell short of the targeted level, it marked a significant 75% increase from the previous year’s auction. Notably, offshore wind comprises more than half of the Philippines’ future utility-scale renewable capacity, with a fivefold increase over onshore wind. Following an executive order issued in April 2023 to foster cooperation between private investors and the government on offshore wind projects, contracts in this sector have more than doubled, now representing 61GW.

Laos is ambitiously positioning itself in the renewable energy sector, aiming to develop over 3GW of utility-scale solar and wind capacity, rivaling Thailand and surpassing Malaysia’s capacity by more than 150%. This ambition, driven by financial collaboration with ASEAN partners, has positioned Laos to host the region’s largest onshore wind farm – the Monsoon wind farm, currently under construction with an expected capacity of 600MW.

Towards Renewable Ambitions

Despite the large pipeline of wind and solar projects in ASEAN, only 6.3GW, or 3%, is currently under construction. GEM suggests that the target for renewables to constitute 35% of ASEAN’s electricity generating capacity by 2025 is attainable and potentially conservative. With renewables already accounting for 32% of electricity capacity, adding 17GW by 2025 – of which 6.3GW is already underway – could see the region surpass its target. The region has over 220GW of prospective utility-scale solar and wind capacity in development, with 23GW expected to be operational by 2025.

Fossil fuels remain dominant in the region’s energy mix. Gas and coal each account for about 30% of ASEAN’s total installed capacity, with coal power capacity growing by an annual rate of 7% since 2017. Given the current pace of electricity demand growth outstripping renewable energy capacity rollout, gas and coal are projected to continue expanding in the coming years. National energy policies have often positioned gas as a transitional energy source, and ASEAN countries are likely to become net gas importers by 2025. Additionally, inadequate grid infrastructure investment remains a significant challenge for integrating utility-scale solar and wind.

This regional shift towards renewable energy, while promising, highlights the critical role of sustained and adaptive policy frameworks in accelerating and maintaining the momentum in the transition to renewable energy sources.

Lead image courtesy of huangyifei from Getty Images

You may also be interested in :

Southeast Asia’s Biggest Floating Solar PV : Indonesia’s Renewable Powerhouse For 50,000 homes